Acorn’s Chief Education Officer Jennifer Barrett shares her own “wake up’ call’ when she learned to think like a breadwinner, and gives us specific strategies to build wealth and create a path to have the rich life we all deserve.

Jennifer’s Money Lesson-

I think every woman would benefit from thinking like a breadwinner, from really basing our choices, the choices we make with our money and our career on the assumption that we should be able to provide the life that we want for ourselves without having to depend on someone else. If we make our money and career choices on that assumption, we will set ourselves up really nicely. Then if we need someone, whether or not we end up being the main earner is sort of irrelevant, but the most important thing is to think about what do I want in my life and what do I need to do financially, professionally to make that happen? One of the most important pieces of that is building wealth. So that means investing right off the bat as early as you can, as much as you can, because that is really the ticket to freedom. The more money that you have invested, the more freedom you have, because you are decreasing your dependency on each paycheck with the amount of money that you have growing for you. It just gives you so many more options. It means you can buy a house on your own, whether or not you're with somebody else. It means that if you lose a job, you are fine. You have that financial security net. It means if you want to have a baby on your own, you can afford that financially. It just gives you so many more choices with your life.

Jennifer’s Money Tip-

I think it comes down to asking yourself the question, "Are the choices I'm making with my money bringing me closer or further away from the future I want?" That seems like such a basic question, but I still ask myself that a lot of times when I'm thinking about even small choices around my money. "Is this going to bring me closer to the future I want, or is this setting me back?" So it's a good question to ask yourself regularly, a good gut check.

Bobbi’s Tips-

Financial Grownup Tip #1-

Jen talked about how hard it is to negotiate. I've had the toughest time with this too so I want to recommend a book that made a huge difference to me. It's called Never Split the Difference by Chris Voss. He also has a masterclass if you like to watch videos and I can tell you, I watched it all and it is excellent.

Financial Grownup Tip #2-

Thinking like a breadwinner sadly is not optional. I have twice become the family breadwinner totally out of the blue and it was temporary, but let me tell you, it is a shock to the system. Like Jen, I never thought it would happen to me. You don't have to be the breadwinner, but you do have to be ready to step up if life throws you a curve ball. Jen's book will help you do just that, so definitely pick up a copy of Think Like a Breadwinner.

Get your copy of Think Like A Bread Winner by Jennifer Barrett

Follow Jennifer!

Instagram - @jbarrettnyc

Twitter- @jbarrettNYC

LinkedIn- Jennifer Barrett

Website- www.jenniferbarrett.com

Follow Bobbi!

Instagram - @bobbirebell1

Twitter- @bobbirebell

LinkedIn- Bobbi Rebell

Website- http://www.bobbirebell.com/

Did you enjoy the show? We would love your support!

Leave a review on Apple Podcasts or wherever you listen to podcasts. We love reading what our listeners think of the show!

Subscribe to the podcast, so you never miss an episode.

Share the podcast with your family, friends, and co-workers.

Tag me on Instagram @bobbirebell1 and you’ll automatically be entered to win books by our favorite guests and merch from our Grownup Gear shop.

Full Transcript:

Bobbie Rebell: Question for you guys. Are we ever going to get back to that whole dress up for work thing the way we used to? I don't know. But one thing I do know is it is time to get out of those PJ's and those grungy tshirts, and we need to give ourselves an upgraded, but still super comfy, wardrobe that makes us smile, and ideally makes our coworkers, our friends and our family smile as well. I have so many friends that I've wanted to send a little pick me ups to, to let them know it's all good, and that includes you. So that's why I created Grownup Gear, a fun line of t-shirts, sweats, pillows, mugs, totes, and more thaT I guarantee will give you and everyone that you're Zooming with all day long, a good giggle.

Bobbie Rebell: Grownup Gear is about saying the things out loud that we tell ourselves silently. Like when you wake up and you look in the mirror and you think, "I can't believe I'm a grownup either." Or maybe you just want to be honest that you are still a grownup in progress, or you want to send a gift congratulating a friend for paying off their debt. The most comfy sweatshirts, t-shirts, tote bags, mugs, pillows, and more. Give it to yourself or your favorite grownup, or almost grownup, friend. Go to grownupgear.com to check it out. For discount codes and sales, follow us on Instagram at our new handle, @grownupgear, and DM us with any questions. And thank you because by supporting Grownup Gear, you help support this free podcast.

Jen Barrett: Deep down. I really don't think I believed that I would be taking the lead financially at any point in my life. I really thought my husband would be the main earner. So it probably seemed less important to negotiate that salary, and then for the next seven years, I barely negotiated my raises.

Bobbie Rebell: You're listening to Financial Grownup with me, certified financial planner, Bobbi Rebell, author of How To Be a Financial Grownup. And you know what? Being a grownup is really hard, especially when it comes to money, but it's okay. We're going to get there together. I'm going to bring you one money story from a financial grownup, one lesson, and then my take on how you can make it your own. We got this.

Bobbie Rebell: Hey, Grownups, this episode has been about five years in the making. I'll never forget sitting in a Midtown restaurant with my new friend, Jennifer Barrett. A mutual friend had introduced us thinking, "Well, you guys have a lot in common and maybe you guys will come up with some projects together." So we were brainstorming our two big ideas. For me, it was Financial Grownup and the idea of sharing money stories to inspire people to build the foundation for a wealthy life of choices, getting to live the life that they want. For Jen, it was the concept that we all had to, well, think like breadwinners. Jen had, and still has, I should say, what we call a big job. She really is the breadwinner and her job as the chief education officer at Acorns is intense and sometimes all consuming. But finally, her new book, Think Like a Bread Winner, A Wealth Building Manifesto For Women Who Want To Earn More and Worry Less is coming out.

Bobbie Rebell:I can tell all of you it has been well worth the wait. I was honored that Jen asked me to contribute to this book and to endorse it along with David Bach, Eve Rodsky, the author of Fairplay, Farnoosh Torabi, who by the way wrote When She Makes More, so thinking along the same path, and Erin Lowry, who's been a frequent guest on this podcast, author of the Broke Millennial books series, and many more. In our interview, Jen Barrett shares the story that started it all when she realized what she didn't want to admit. If she wanted to get what she wanted to get, she was going to have to start thinking like a breadwinner. Here is Jennifer Barrett.

Bobbie Rebell: Jen Barrett, you are a financial grownup. Welcome to the podcast.

Jen Barrett: Thanks so much for having me.

Bobbie Rebell: I'm so excited to talk to you about your new book. So many years in the making, we've been talking about this for years. It's finally here. Think Like A Breadwinner, A Wealth Building Manifesto For Women Who Want To Earn More and Worry Less. By the way, Jen, it's already getting reviews that are amazing. This one I'm going to read to people. It's from Ladders, which is a career website. "Jennifer Barrett's manifesto for working women transcends its goal by being more than a finance book, but a testament that anyone anywhere can achieve their goals with the right advice." Not bad, Jen.

Jen Barrett: Yeah, that was a nice review. It was nice to read.

Bobbie Rebell: You're very modest.

Jen Barrett: I know. You're so nervous. You're on pins and needles before the book comes out. You're like, "I hope they like it." So it was really nice to read that.

Bobbie Rebell: Well, I got a sneak peek of the book because I got to endorse it so everyone can read my blurb when they get the book. Before we talk more about it, though, you did bring with you a money story, which really inspired the book so many years ago. Tell us your money story, Jen.

Jen Barrett: Yeah, well, there's a material difference between being able to cover the bills and handle a budgets and building wealth that supports your life and the future you want. That difference became super clear to me just after we'd had our oldest son. At the time, I was in my early 30s and we were sharing a small one bedroom apartment with our toddler who was about 18 months old. One night I was pacing back and forth with him, trying to get him back to sleep, and I think it just hit me so hard in that moment that we were in a situation that was just completely unsustainable.

Jen Barrett: I had this moment of, "Wait a second. I thought I was doing everything right financially." I had a little 401k. I had a little bit of savings. I was paying half the bills. But what I realized was that I hadn't been putting money away for the things that were most important to me, and that was being able to have another child, to afford to buy a place or even to move into a bigger apartments because we lived in Brooklyn, which is not cheap. I did some real soul searching and asked myself, "Why didn't I make those choices with my money to save more and to invest more?" I realized that subconsciously I had been thinking that my husband would take the lead there. In that moment, I think it finally dawned on me how precarious an assumption that is. So I asked myself in the days that followed, "How would the choices I make with my money and my career be different if I had been raised to think like a breadwinner?"

Jen Barrett: That's what sort of set me off on a whole new journey and brought me to where I am today, more than a decade later, which is a much better place financially. We have a larger home. I helped with most of the down payment. We have two lovely sons now. I've had both a career and been able to build the kind of wealth that I couldn't have even imagined 12 years ago when I had that wake up call.

Bobbie Rebell: Tell us more about what you were doing before you had that wake up call, what kind of job you had. Because you had a really good job that a lot of people would be very, very envious of and really admire. I mean, you were high achieving and then the things that you looked for in the next job, besides obviously paying more. I know there was a lot of soul searching about sort of what people would think, because we're both journalist backgrounds, there's a lot of judgment there.

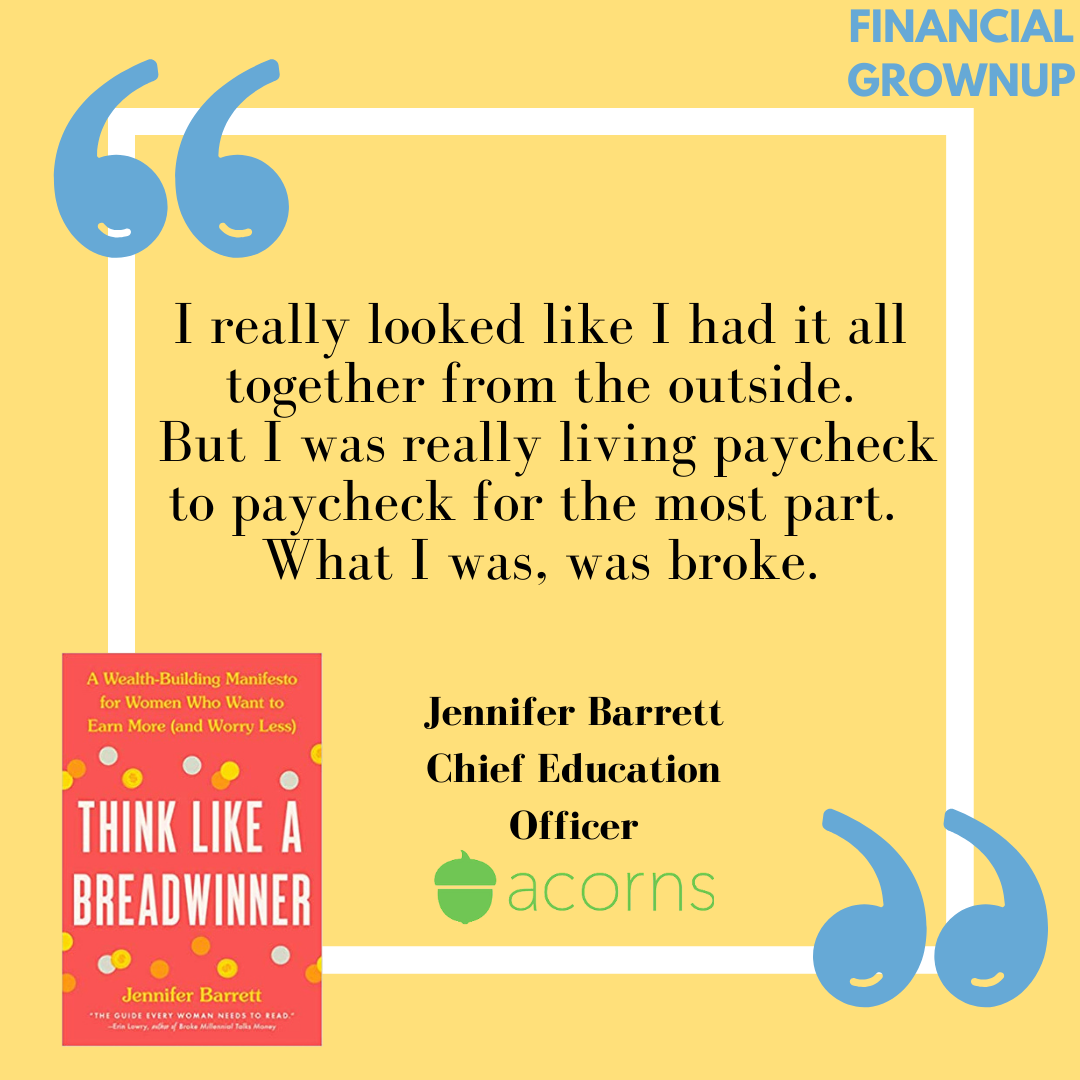

Jen Barrett: Yeah, and I think that's an important point is just because you have a good job doesn't mean that you have your finances together. You can be a professional success and feel like a financial failure. I interviewed more than 100 women for the book and I did find that to be the case with a surprising number of women who were otherwise very successful. So I think I was in sort of the same situation but with one crucial distinction, which is I was an editor at Newsweek at that point a pretty big weekly news magazine. It has since sort of gone under and been reborn and it's not quite the same as it used to be, but it was a great job. I really looked like I had it all together from the outside, but I was really living paycheck to paycheck for the most part.

Jen Barrett: We say paycheck to paycheck, but what I was was broke, right? I only had a few hundred dollars in my savings. I was still paying down some credit card debt. So if you looked at my actual net worth, I was in negative territory and I really wasn't making the kinds of choices or making the kinds of money that would allow me to support the life that I really wanted. One big reason for that, which is almost embarrassing to admit now and I've since changed my approach with this significantly, is that I had never negotiated my salary. So when I got the job at Newsweek, I was just so thrilled to be hired there I literally did not even think to negotiate. I do think part of that was that I was so excited to be hired there, but the other part of it was deep down I really don't think I believed that I would be taking the lead financially at any point in my life.

Jen Barrett: I really thought my husband would be the main earner and so it probably seemed less important to negotiate that salary. Then for the next seven years, I barely negotiated my raises. So one other critical moment for me was I came back from maternity leave and I found out that someone had been hired who had just a few more years experience than me in a very similar role and they were making 50% more than me. That moment was like ... It was so crushing that I vowed I would never ever make that mistake again and I was going to negotiate the hell out of every job offer and raise that I got from that point on, and it made me sort of reassess this idea I had about loyalty and about employers just taking care of you because you're doing a great job. It was a real wake up call in that sense too, where I realized I need to advocate for myself. I need to show my value. I need to ask for it and not assume that I'm going to get it just because I'm doing a good job.

Bobbie Rebell: So you set out to get a job that paid more. Tell us what that job was and how that onboarding went.

Jen Barrett: Yeah. So I was hired in my first job in management. I became the director of a health site. It was part of NBC. It was called iVillage Health. It was a huge site at the time. I think one of the top five largest health sites for women. It was a dramatic increase in the amount of responsibility I had, but also in my salary. So I ended up making almost double what I had ... Actually, no. More than double what I had been making at Newsweek and in between there I freelanced, and when I was freelancing, I really understood that I had undervalued myself and my skills because I was able to make a lot more freelancing than I had in my full-time job at Newsweek. So that was also a realization and a validation of the fact that the skills that I had were valuable. Then with this job, it both provided a lot more income. It allowed me to get the mortgage and it also put me on the management track, which I have been on ever since.

Bobbie Rebell: Jen, what was your husband thinking while this was going on? Did you have talks about this?

Jen Barrett: We did and I think part of it was when he and I first started dating, he was working at a startup at the time and was making a lot more than I was as a reporter. But I think that's where some of the assumptions sort of got set in my head. The startup went under and then he moved back to journalism. So he took a pretty big pay cut and suddenly our salaries were much closer than they have been. But I think in my head, I still kept telling myself that that was a temporary situation. I still expected him to earn considerably more than me, even as the evidence started to mount that that may not be the case, particularly with both of us being in journalism. We did have some discussions around that and in particular, when I got that job in management at that point, he was on contract.

Jen Barrett: So we realized that my income and my income prospects were probably greater at that particular point. Certainly I was the one who had secured the mortgage in part because I had a full-time job and it's very difficult when you are on contract to get approved. So we realized that my income was really critical to the household and so that launched a whole series of discussions about how is this going to work. I'm not going to say it was easy. We had to have a lot of really difficult discussions because I was pregnant with our second son when I moved into the breadwinner role. In my mind, again, I thought, "Oh, this is sort of a temporary situation where I'm going to take on this really demanding role so we can get the mortgage. I'll keep doing this."

Jen Barrett: Then I found I really enjoyed it. I realized I really am quite ambitious and so I wasn't sure I wanted to give up that role, but at the same time, for a while I was also trying to be the primary caregiver and that, as anyone who has tried to do both can tell you, is almost impossible to sustain. So it led to some really emotional and candid conversations with my husband about what role are we each going to take here and how are we going to divide all the responsibilities, household responsibilities, caregiving, breadwinning, in a way that feels fair to each of us?

Bobbie Rebell: Jen, what is the lesson from your story?

Jen Barrett: I think every woman would benefit from thinking like a breadwinner, from really basing our choices, the choices we make with our money and our career on the assumption that we should be able to provide the life that we want for ourselves without having to depend on someone else. If we make our money and career choices on that assumption, we will set ourselves up really nicely. Then if we need someone, whether or not we end up being the main earner is sort of irrelevant, but the most important thing is to think about what do I want in my life and what do I need to do financially, professionally to make that happen? One of the most important pieces of that is building wealth.

Jen Barrett: So that means investing right off the bat as early as you can, as much as you can, because that is really the ticket to freedom. The more money that you have invested, the more freedom you have, because you are decreasing your dependency on each paycheck with the amount of money that you have growing for you. It just gives you so many more options. It means you can buy a house on your own, whether or not you're with somebody else. It means that if you lose a job, you are fine. You have that financial security net. It means if you want to have a baby on your own, you can afford that financially. It just gives you so many more choices with your life.

Bobbie Rebell: You also brought with you in everyday money tip.

Jen Barrett: Yeah, I think it comes down to asking yourself the question, "Are the choices I'm making with my money bringing me closer or further away from the future I want?" That seems like such a basic question, but I still ask myself that a lot of times when I'm thinking about even small choices around my money. "Is this going to bring me closer to the future I want, or is this setting me back?" So it's a good question to ask yourself regularly, a good gut check.

Bobbie Rebell: It's a very good gut check and I think it's something that sounds easy, but we don't really do that a lot. We don't usually just kind of pause and sit down and really think about that and maybe even write down a few things that we want to do. I find when you write things down, sometimes they stick a little bit better. I don't know. All right, we got to shift gears because I don't want to run out of time and we have to talk about Think Like A Breadwinner because this is a book that has been in the making for quite a long time, because it is so well researched, Jen. You spent a lot of time doing the work here and the book is chock-full of statistics that are ... Some of them would just blow my mind. If you could share with us just one statistic that's sort of your elevator pitch to get this book, what is that one stat that stands out?

Jen Barrett: Well, I think one of the most significant stats is that half of moms in this country today are contributing at least 40% of the total household earnings. That's according to the latest Institute for Women's Policy Research report. That just reinforces the fact that women's income is absolutely critical right now. I think we saw that when women started dropping out of the workforce. We could see what the impact was going to be, not just on families, but on the economy.

Bobbie Rebell: A lot of this book was already done before the pandemic, but you were still finishing it up during the pandemic. What is in the book now that would not have been pre-pandemic?

Jen Barrett: The pandemic reminded us of how important it is to take charge of our finances and to build the kind of savings and wealth that provide financial security and help us weather tough times like this. So that message of taking care of yourself and putting money into an investment account and building wealth to support you not just now but in the future is more important than ever.

Bobbie Rebell: So well said. Jen, where can people catch up with you? I know that your book is going to be everywhere.

Jen Barrett: I hope so. You can find me at jenniferbarrett.com and you can read more about the book there, and then I'm on social media all over the place. It's @jbarrettNYC on Instagram, Twitter. I'm on LinkedIn.

Bobbie Rebell: All the places.

Jen Barrett: Oh, the places. Clubhouse. Yes.

Bobbie Rebell: Yes, Clubhouse. Let's not forget that. Thanks, Jen.

Jen Barrett: Thank you.

Bobbie Rebell: Here we go. Financial Grownup tip number one. Jen talked about how hard it is to negotiate. I've had the toughest time with this too so I want to recommend a book that made a huge difference to me. It's called Never Split the Difference by Chris Voss. He also has a masterclass if you like to watch videos and I can tell you, I watched it all and it is excellent. Financial Grownup tip number two, thinking like a breadwinner sadly is not optional. I have twice become the family breadwinner totally out of the blue and it was temporary, but let me tell you, it is a shock to the system. Like Jen, I never thought it would happen to me. You don't have to be the breadwinner, but you do have to be ready to step up if life throws you a curve ball. Jen's book will help you do just that, so definitely pick up a copy of Think Like a Breadwinner.

Bobbie Rebell: One thing I do, I always try to think of new revenue streams. My latest is Grownup Gear. You can see more about it at grownupgear.com. I hope you'll support it by checking out the merchandise. It's perfect for all of your grownup milestones. Gifts for graduation, new parents, mother's day, father's day, a new home, birthdays, or just celebrating being a grownup and kind of owning it. Discount codes available on my Instagram @bobbirebell1. Another reason to follow me on Instagram, we will be giving away copies of Jen's book and of other authors on the show. This spring, so many amazing authors are on tap and they're generously giving gifts to our Grownup community. I also want to invite everyone to join our weekly Friday at 1:00 PM Clubhouse chats in the Money Tips For Grownups club. DM me on Instagram if you need and invite to Clubhouse. Big thanks to Jen Barrett for helping us all be financial grownups.

Bobbie Rebell: The Financial Grownup Podcast is a production of BRK media. The podcast is hosted by me, Bobbi Rebell, but the real magic happens behind the scenes with our team. Steve Stewart is our editor and producer, and Amanda Savan is our talent coordinator and content creator. So yeah, that means she does the show notes you can get for every show right on our website and all the fantastic graphics that you can see on our social media channels. Our mission here at Financial Grownup is to help you be at your financial best in every stage of life. This year we want to help you get there by giving away some of our favorite money books.

Bobbie Rebell: To get yours, make sure you are on the Grownup list. Go to bobbirebell.com to sign up for free. While you're there, please check out our Grownup Gear shop and help support the show by buying something to express your commitment to being a financial grownup. Stay in touch on Instagram @bobbirebell1and on Twitter @bobbirebell. You can email us at hello@financialgrownup.com and if you enjoyed the show, please tell a friend and maybe leave a review on Apple podcasts. It only takes a couple minutes. Join us next time for more stories to help you live your best grownup life.